Years ago, the concept of trading carbon credits seemed distant and impractical. However, recent developments have brought forth a detailed blueprint for establishing a sustainable and transparent carbon credit market.

During times of uncertainty and budgetary constraints, one might expect that companies’ voluntary carbon credits purchase would decline. However, the growth of the voluntary carbon market suggests otherwise. The voluntary carbon market grew 4 times in value to ~$2bn as compared to 2020 as per BCG study. This growth underscores the market’s growing credibility and significance.

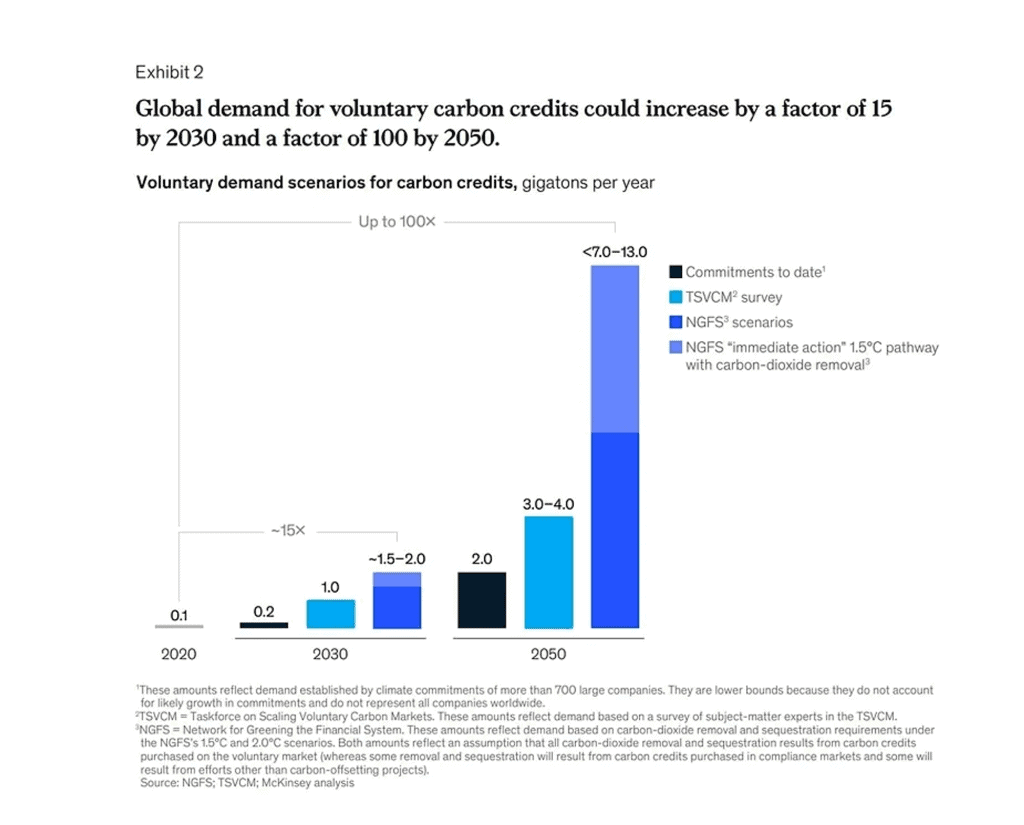

The exciting part? The voluntary carbon market is predicted to see a boom: a steep 15-fold increase or more in demand for carbon credits by 2030, and a staggering increase of up to 100 times by 2050. This surge, in turn, could lead to a market worth over $50 billion by 2030 as per McKinsey study. Significant for both, our increasingly fragile environment, and the future of our business landscape, a key takeaway has emerged – The time has come to consider environmental sustainability as an integral facet of your business strategy, and the emergent carbon credits market is an avenue worth exploring.

Role of Carbon Credits in Achieving Climate Targets

Carbon credits offer a pathway for companies to achieve their climate-change objectives. More companies are aligning themselves with the 2015 Paris Agreement agenda to limit the temperature rise to 2°C above pre industrial levels, and preferably 1.5°C.

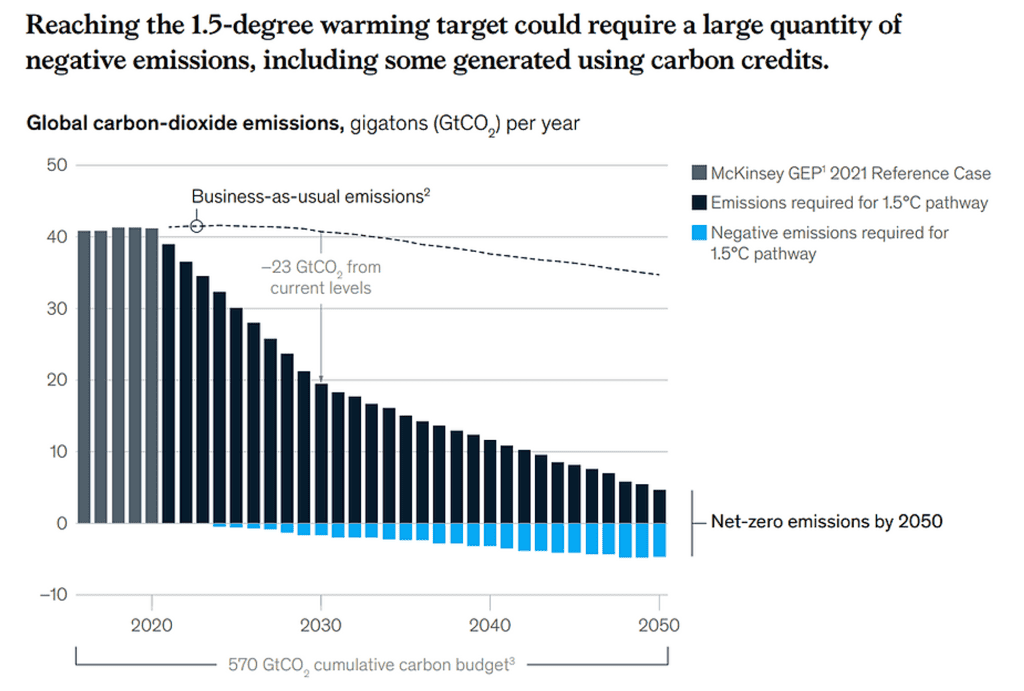

To attain the ambitious net-zero target worldwide, companies must strive to reduce their own emissions significantly. Nevertheless, achieving net-zero emissions is unattainable for any company due to the presence of unavoidable emissions inherent to each sector.

In light of these challenges, achieving emissions reduction in line with a 1.5°C net zero target necessitates the utilization of carbon offsets, achieved by removing greenhouse gases from the atmosphere.

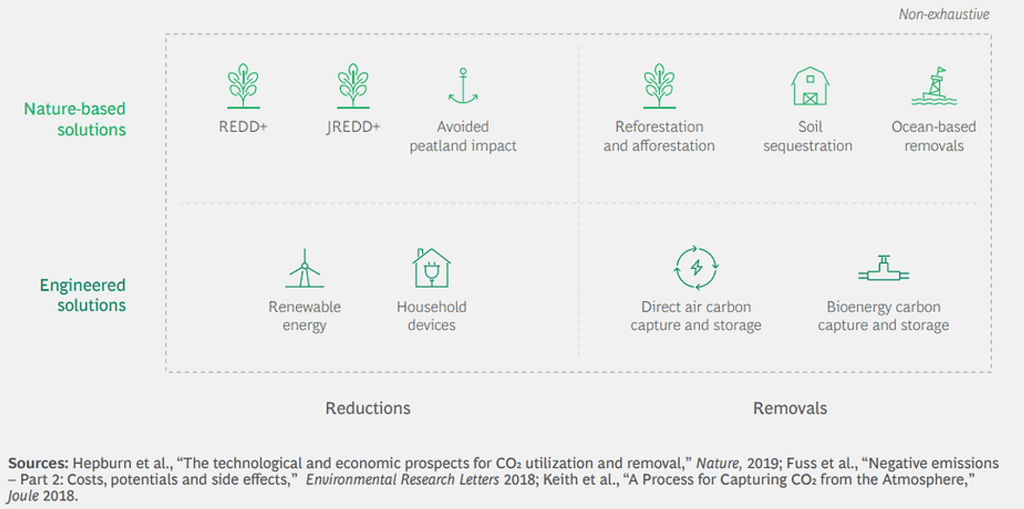

Each project or program adopts one of the following two broad approaches to generate impact:

Reduction: Reduction, also known as avoidance credits entail preventing or reducing the emission of a metric ton of CO2 into the atmosphere. Examples include nature-based solutions (NBS) such as avoiding deforestation, or technology-based solutions like generating renewable energy that displaces fossil fuel generation.

Removal: Removal credits involve the extraction of CO2 from the atmosphere, achieved through nature-based solutions like biochar production or ecosystem restoration, or technology-based solutions such as Direct Air Capture (DAC). Removal projects directly reduce the concentration of carbon in the atmosphere by eliminating historical emissions.

Source: BCG Report (The voluntary carbon market: 2022 insights and trends)

In recent years, there has been a noticeable trend towards favoring removal credits, which has been widely observed. Discussions regarding the comparative advantages of reduction and removal credits are gaining traction among different stakeholders.

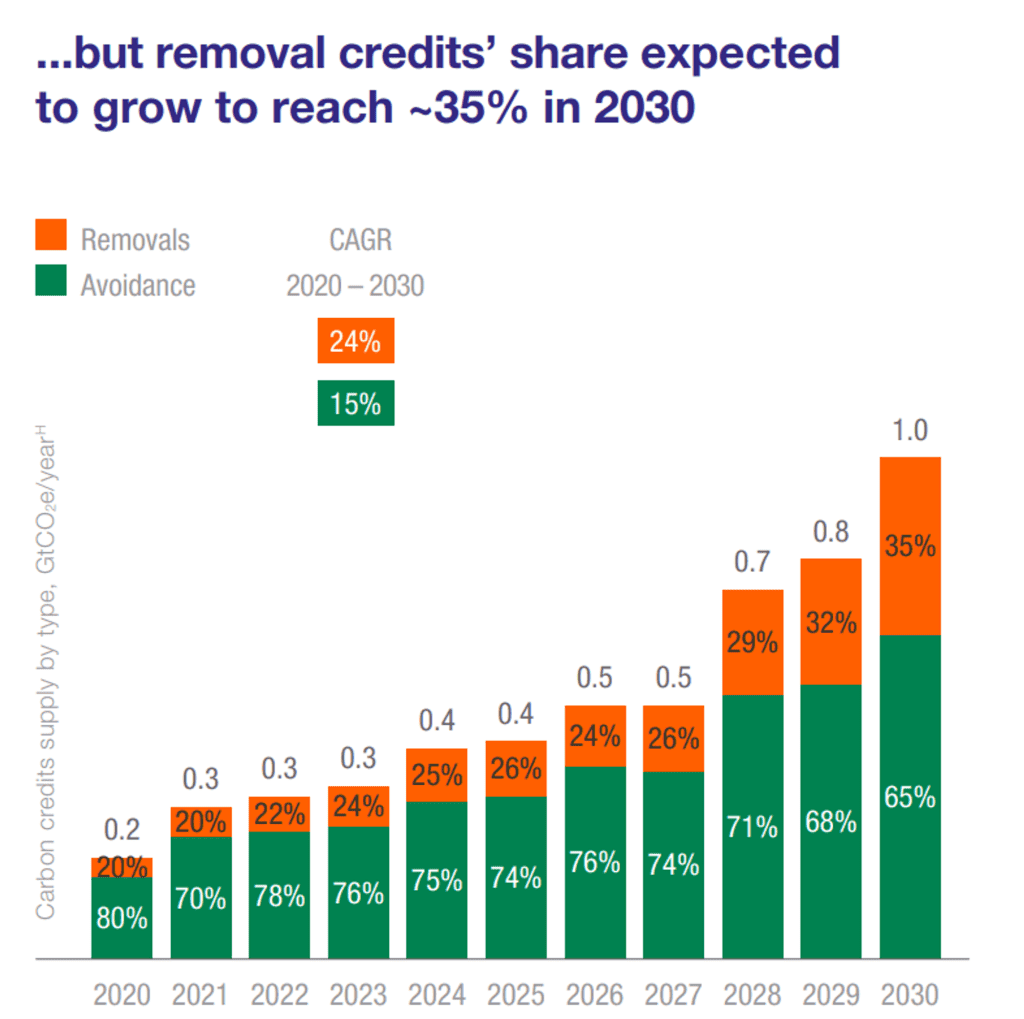

Since 2015, reduction credits have dominated the market, comprising over 80% of market share, and are projected to reduce its share to approximately 65% by 2030.

On the other hand, removal credits have held a minority share of less than 20% since 2015, but are anticipated to increase to 35% by 2030. This growth is propelled by advancements in technologies and methodologies, improved affordability, and the increasing demand for net-zero initiatives.

Source: BCG Report (The voluntary carbon market: 2022 insights and trends)

Quality Challenges

While the voluntary carbon market experiences significant growth, it’s crucial to acknowledge the existence of various quality challenges associated with both reduction and removal projects. Therefore, conducting a thorough quality assessment of any project before purchasing becomes imperative.

By carefully evaluating projects against the following six primary criteria and prioritizing according to their unique needs, buyers can confidently navigate the market and choose projects that align with their goals and values.

Measurement, Reporting, and Verification (MRV): Projects must adhere to robust principles, provisions, and methodologies for quantifying emissions reductions and removals. It’s crucial that quantified emissions are not overestimated.

Permanence: Considers how long the removed carbon will stay out of the atmosphere. For example, carbon capture and storage (CCS) technologies offer a permanent solution by storing carbon underground. Conversely, forestry projects may face risks like fires or logging, which could release sequestered carbon back into the atmosphere.

Additionality: This refers to whether the reduction of greenhouse gas emissions would have occurred without the carbon market’s influence. If emissions reductions are not additional and would have happened anyway, purchasing carbon credits then becomes useless.

Vintage: Vintage credits refer to credits released in previous years that were not retired. While leftover credits don’t necessarily indicate inferior quality, an inability to sell most credits may signal underlying issues with a project.

Co-benefits: Evaluate the broader impact of the project beyond carbon removal. High-quality projects provide benefits such as clean water, habitat preservation, and livelihood opportunities for local communities. Additionally, consider how the project aligns with various Sustainable Development Goals (SDGs) beyond carbon offsetting.

Leakage: Assess the risk of displacing activities that could shift emissions from the project to another location. Leakage occurs when a reduction in emissions in one area leads to intensified emissions elsewhere, resulting in no net reduction overall.

As per a survey conducted by BCG, 91% of buyers prioritize the monitoring, reporting, and verification framework (MRV) metric the most amongst the above six listed criteria while making credit purchase decisions. Buyers aim to ensure that the credits they acquire deliver measurable benefits, driven by concerns regarding the reputational repercussions of purchasing ineffective credits.

Conclusion

The carbon market experienced remarkable growth in recent years, witnessing increase in value for both compliance and voluntary markets compared to 2020.

Discussions surrounding the reduction versus removals dilemma are gaining traction, yet solutions are not black and white. Given the magnitude of climate action required, both strategies are imperative on a large scale – encompassing efforts such as reducing deforestation, enhancing natural ecosystem restoration, promoting regenerative agriculture, and implementing technological removal solutions.

These trends, seen in the carbon markets, emphasize the importance of carbon offsets and a stern focus on its quality. After all, confidence in quality can shift market dynamics and redefine values.

Note: Carbon offsets alone can’t achieve decarbonization. To achieve decarbonization, it’s crucial to focus on reducing emissions right from the start. Carbon offsets should complement these efforts, not replace them.

FAQs

What is the carbon offset market?

The carbon offset market enables companies and individuals to compensate for their greenhouse gas emissions by purchasing credits from projects that reduce or remove CO₂ from the atmosphere. These projects include renewable energy initiatives, reforestation, and carbon capture technologies.

How has the voluntary carbon market grown in recent years?

The voluntary carbon market has expanded significantly, growing fourfold to approximately $2 billion compared to 2020. Projections indicate a potential market value exceeding $50 billion by 2030, driven by increased demand for carbon credits.

What are the main types of carbon credit projects?

Carbon credit projects are categorized into reduction (avoidance) and removal. Reduction projects prevent emissions, such as through renewable energy or forest conservation. Removal projects extract CO₂ from the atmosphere, utilizing methods like biochar production or direct air capture.

Why are carbon credits important for achieving climate targets?

Carbon credits assist companies in offsetting emissions that are challenging to eliminate, supporting global efforts to limit temperature rise in line with the Paris Agreement. They are integral to strategies aiming for net-zero emissions.

What challenges does the carbon offset market face?

Despite growth, the market faces challenges such as ensuring the quality and transparency of carbon credits. Concerns include verifying the actual impact of projects and preventing issues like double-counting or greenwashing.