In recent years, businesses have come leaps and bounds in how they approach their responsibilities towards society and the environment. With increasing scrutiny from stakeholders and regulatory bodies, the importance of Business Responsibility and Sustainability Reporting (BRSR) cannot be overstated.

In May 2024, the Securities and Exchange Board of India (SEBI) issued a circular that brings into light the common mistakes and discrepancies that companies have made while preparing Business Responsibility and Sustainability Reporting (BRSR). Consider this circular a wake-up call for companies to improve their sustainability reporting and provide more accurate, consistent, comparable and useful information to investors and stakeholders.

SEBI’s circular has identified several critical issues and mistakes observed in BRSR submissions of many companies. They have even singularly pointed out some of the most common errors, a step which shows just how seriously the BRSR may now be scrutinised.

One of the striking observations is the lack of expertise in handling sustainability-related data, particularly in Principle 6. This principle requires companies to disclose their environmental data, including energy consumption, greenhouse gas emissions, and water usage. However, many companies may lack the necessary expertise to collect and report this data accurately, leading to wide divergence in emission disclosures and asymmetry within the same industry.

On top of that, several entities have even failed to report data in prescribed units, which can put a company’s reliability in question. This not only makes it difficult to compare companies’ sustainability performance but also hampers identification of trends and patterns.

Upon reviewing the company’s sustainability report, several other discrepancies were identified. For instance, data inconsistency, incomplete and missing disclosures and misinterpretations of the guidelines are some of the most commonly occurring errors.

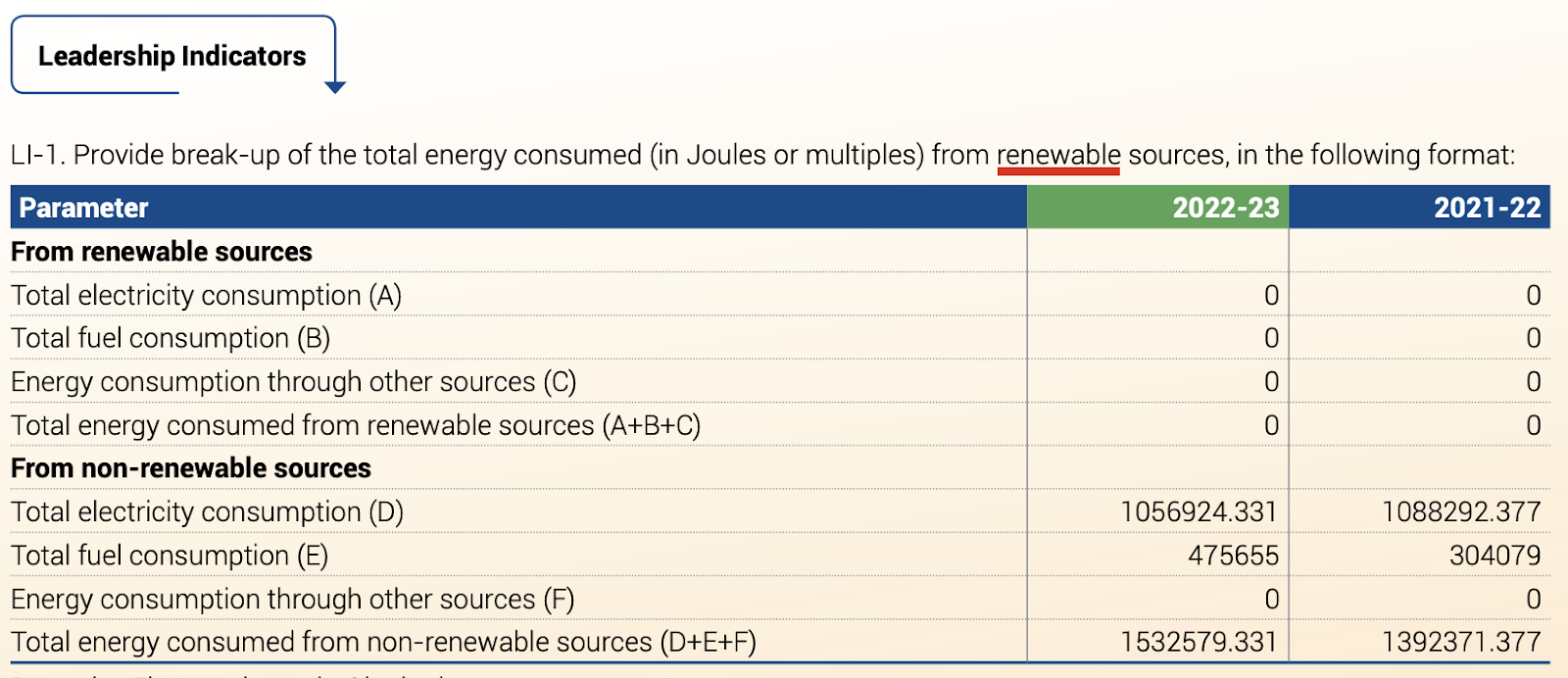

Errors in data collection and reporting can lead to inconsistencies in how metrics are measured and reported. For example, a company has disclosed zero energy consumption from renewable sources in the first table and reported 2,21,405.21 GJ in another table.

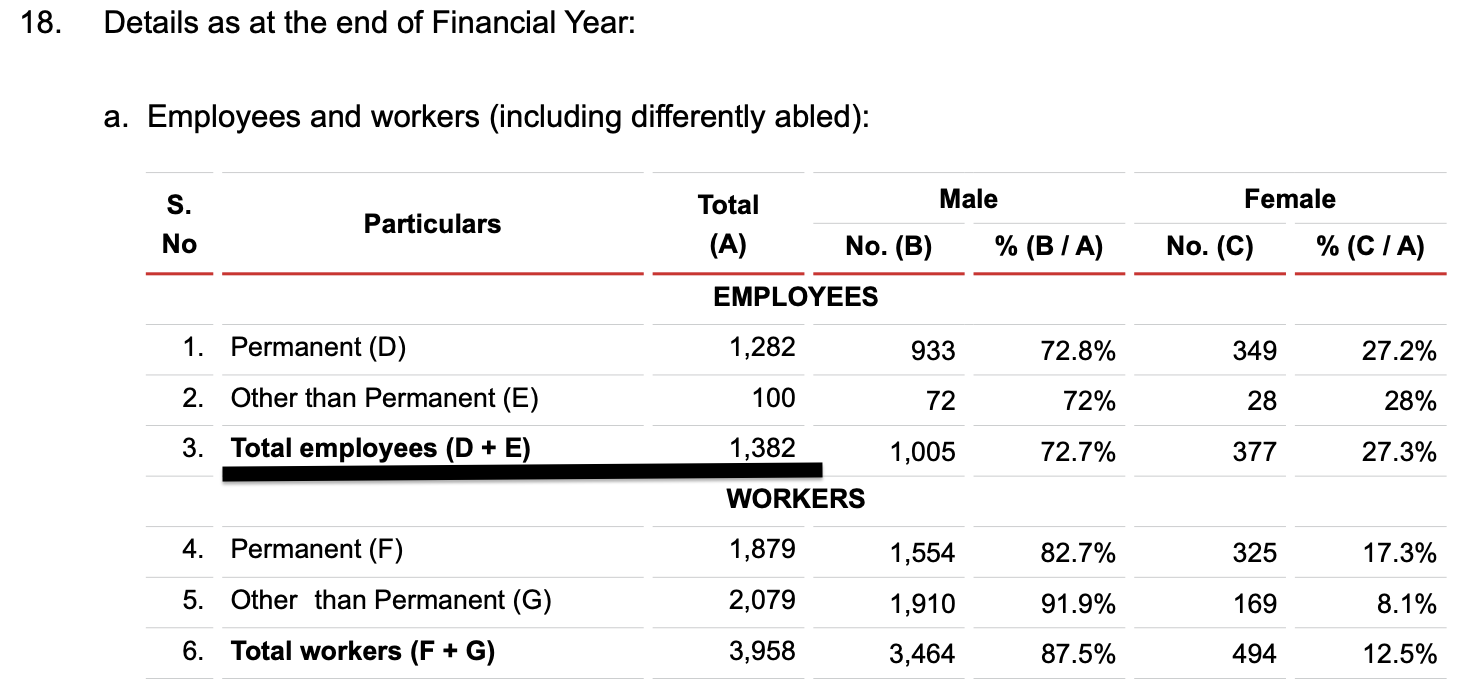

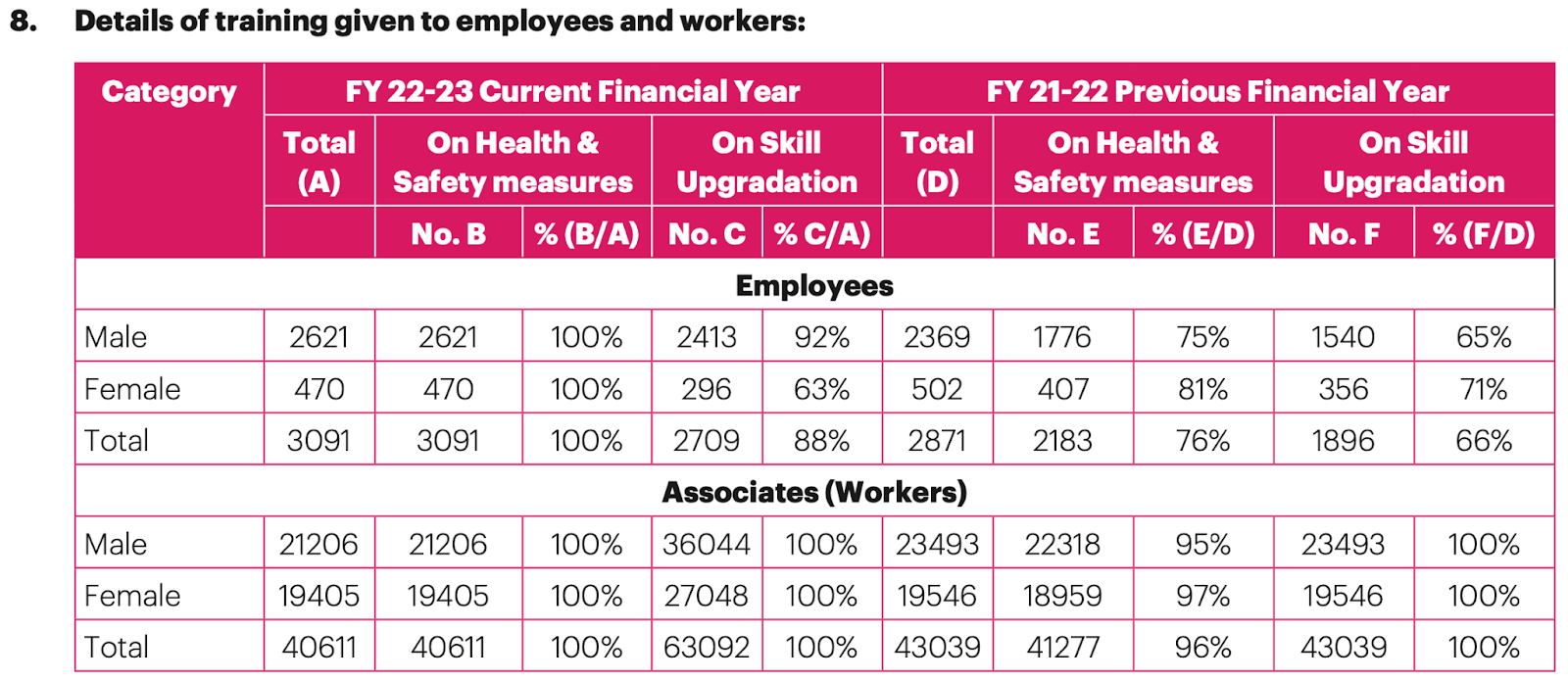

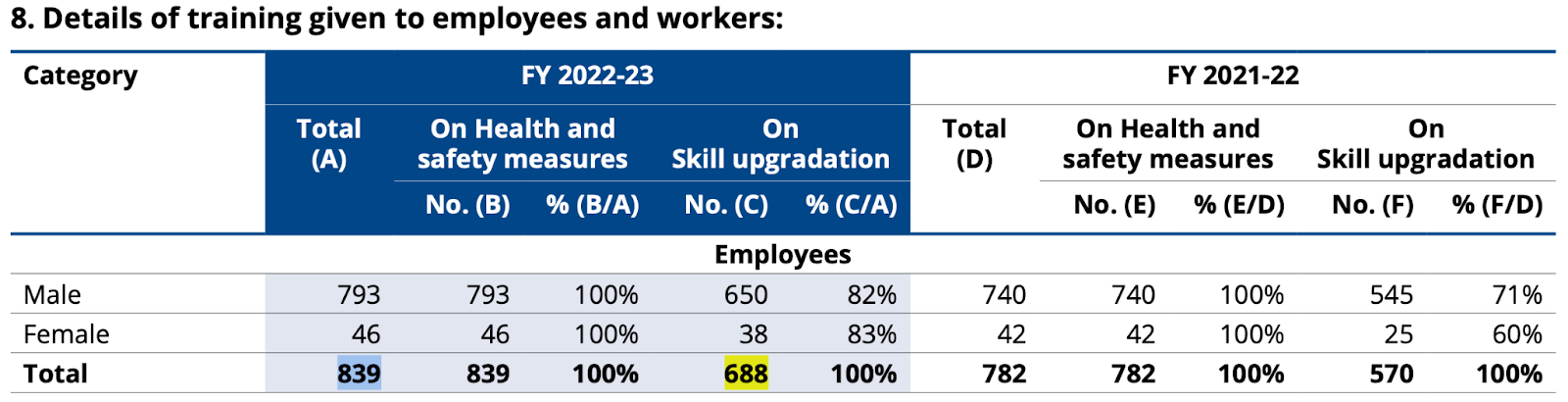

There are even inconsistencies in the total employee count, with mismatched numbers reported in different sections of the report.

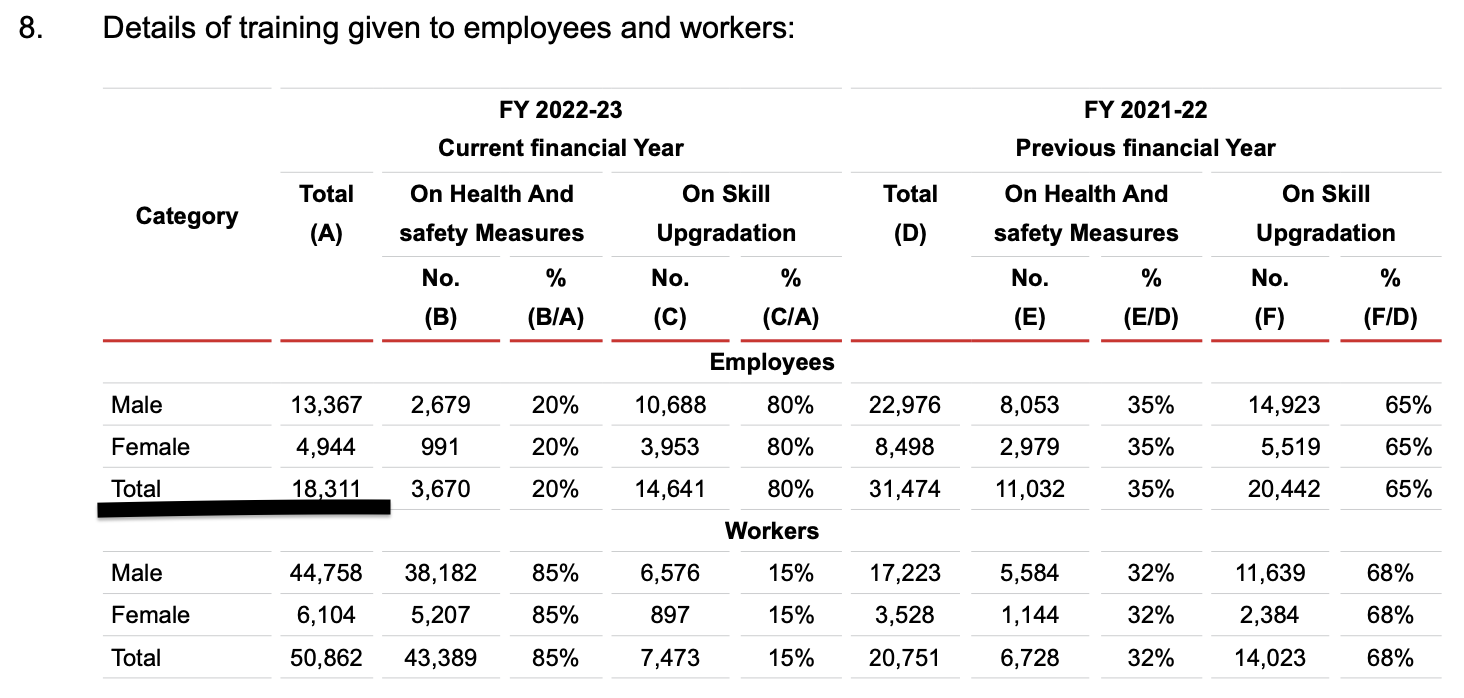

There are issues such as a company claiming to have provided training to more workers than its total strength, with some sections reporting 100% training participation, which is simply quite unlikely.

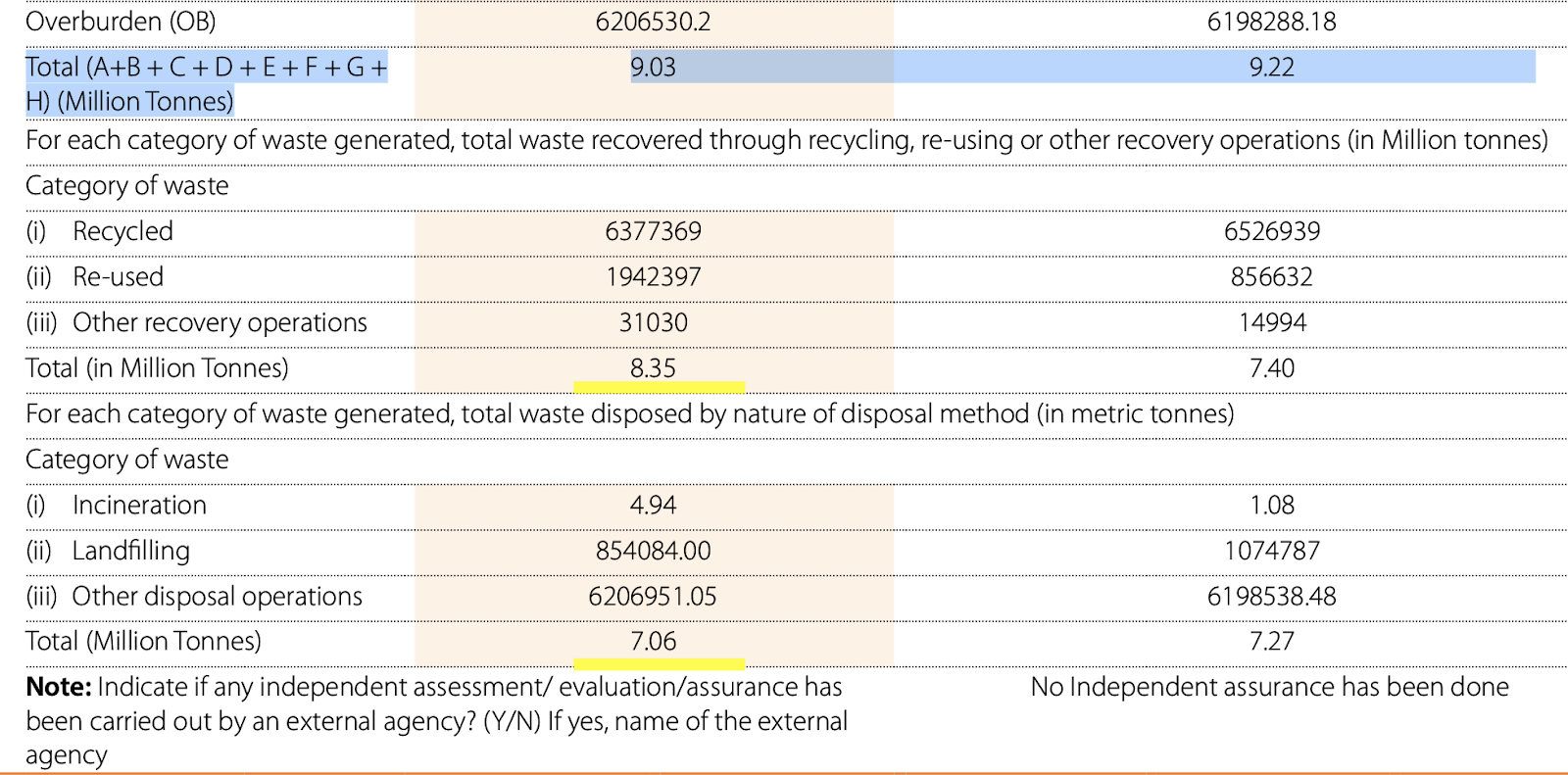

Another company reported a higher amount of waste recovered and disposed than waste generated.

Missing or inadequate data, such as a company entirely omitting energy consumption figures for two years, not only hinders transparency but also raises serious concerns about a company’s commitment to sustainability.

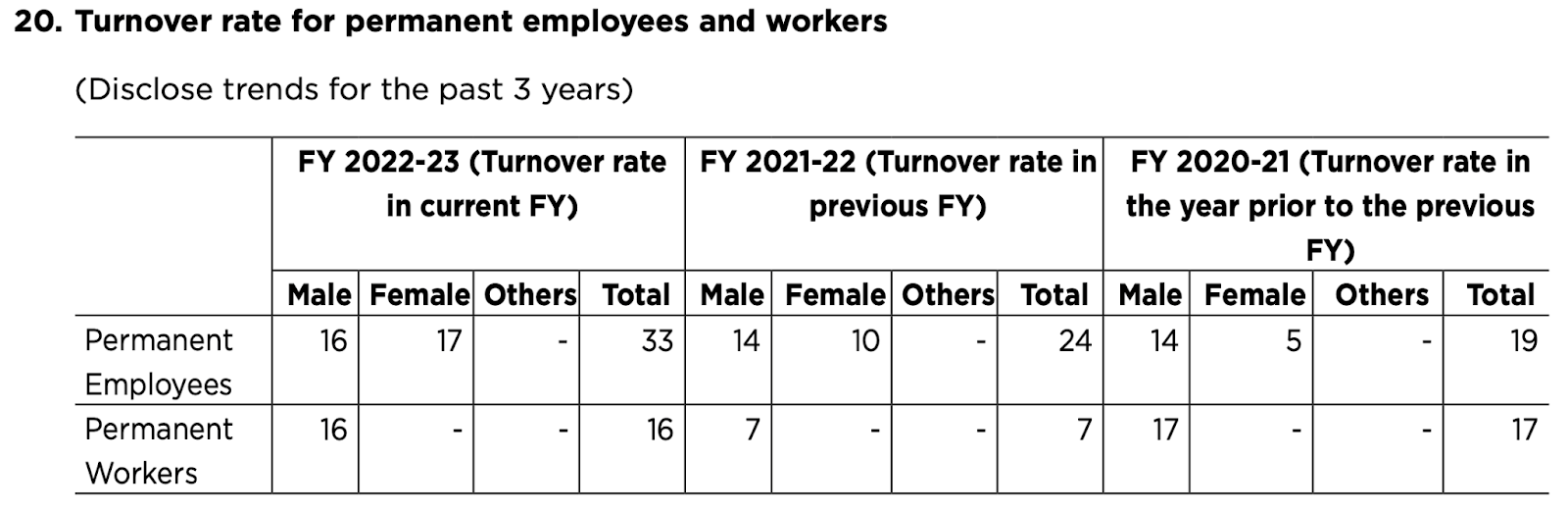

Inaccurate application of BRSR guidelines also results in misleading sustainability reports. For instance, an entity had reported the overall turnover rate instead of the actual employee turnover, which can lead to an inflated or deflated sense of employee retention.

To address these discrepancies SEBI has emphasised on certain specifications for companies to improve their sustainability reporting.

SEBI’s circular is a call to action for companies to enhance their sustainability reporting. The circular can be seen as a significant step towards promoting transparency and accountability in sustainability reporting, and companies must take it seriously to avoid risks of any sort.

The implications of the circular can be far-reaching. Companies that fail to comply with the guidelines may face reputational and financial risks. On the other hand, companies that do comply with the guidelines to improve their sustainability reporting can have

At Sprih, we recognize the challenges companies face in meeting these requirements and offer a comprehensive solution to help you achieve compliance with confidence. Preparing a sustainability report can be daunting; there are multiple layers to the BRSR that can make the process tedious, cause delay in publishing and demand too much manual work. You might want to consider leveraging technology to help you perfect your BRSR or any other framework based sustainability report.

Don’t let inconsistencies undermine your credibility – talk to our expert today and schedule a demo to discover how Sprih can support your BRSR journey.